By Phillip Ng, VP of Corporate Development

Over the last month, the price of Bitcoin has swung wildly. In this environment, Bitcoin miners are undertaking big risks for the opportunity to achieve considerable profits. Or, are they?

Cryptocurrency mining is the computing mechanism that allows for digital currency networks to exist without a trusted third party. This process rewards network nodes (“miners”) for solving a computational puzzle that verifies and records transactions. The economic incentives built into the process are the key innovation that distinguishes cryptocurrency from other digital transactions.

Cryptocurrency mining has become a big business. Bitcoin miners earned over $15 billion in 2021. Miners have raised significant capital to purchase computing hardware and deploy the infrastructure necessary to mine.

This blog will explore the frameworks for mining and demonstrate that investors in cryptocurrency mining, like investors in any industry, are driven by the basic economic forces of supply and demand. They can and should anticipate that the industry will produce long-term yields commensurate with risk.

In the case of the Bitcoin mining market, this means that a series of interconnected factors will drive a return to equilibrium over the long term.

While we have used Bitcoin in our analysis, these principles should apply to any proof-of-work mining markets.

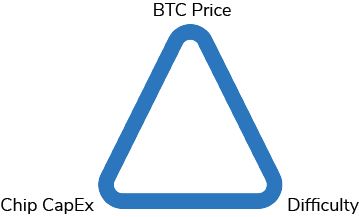

The Golden Triangle

Three inputs determine a miner’s returns and margins:

- Cryptocurrency price levels: The market value of the cryptocurrency rewarded to a miner.

- Difficulty: The probability that a network node will solve the “blockchain puzzle” or “hash puzzle” during the process of adding a new block to the blockchain. Difficulty is algorithmically determined and increases as overall network computing power increases. This factor is designed to steady block rewards and to force adherence to a planned total minting period.

- Miner cost inputs: The costs a miner pays to generate the requisite computing power. Electricity is the main operational cost, varying from miner to miner. Initial capex cost is hardware procurement, which can be quite significant.

By understanding the interplay between these inputs, we can develop a framework for analyzing miners and scoring them against one another.

At Soluna, we refer to this as the “Golden Triangle,” with each input representing one point on the triangle.

The Golden Triangle drives returns to equilibrium in the mining market despite the volatility we observe in the price of Bitcoin (which is driven by macroeconomic forces).

How the Golden Triangle is Maintained

Understanding the triangle inputs illuminates the economics of mining. Consider the following:

1: MINERS HAVE LIMITED SHORT-TERM RECOURSE TO SHIFTS IN ASSET PRICES

- Miners are price-takers of the crypto assets they generate. One Bitcoin is no different than any other Bitcoin. Miners have only two options with regard to the mining process: produce or don’t. Mining hardware prices are a significant upfront capital cost to mining, and represent a sunk cost once purchased.

- Miners will continue to mine so long as the marginal profit from mining exceeds the marginal operating costs. Miners will reinvest capital in equipment, however, only if the expected return on mining exceeds its risk-adjusted return. Some miners will eventually exit the market in adverse price environments.

- Conversely, miners will expand their compute footprint in periods when expected returns well exceed cost of capital.

2: NETWORK DIFFICULTY DYNAMICALLY RESPONDS TO COMPUTE LEVELS

- The Bitcoin network’s difficulty level resets for every 2,015 blocks generated so that the rate of block generation is maintained on average at 10 minutes per block. This mechanism was created to allow the network to compensate for changes in computing power and network participation and ensure a steady minting of coins over 130 years.

- Increased total network computing power results in higher difficulty and lowers expected return per unit of compute input. Conversely, lower network computing power raises expected return per unit of compute.

- Higher price levels mean more participants, which raises difficulty, which lowers average profits back to an equilibrium level. In the long run, lower profits will cause miners to exit, which results in lowered difficulty, raising average miner profit levels.

- The total compute network increases and decreases as a result of the miner’s expected return. The level of mining difficulty tends to revert to maintain a relatively constant level of profitability for miners.

3: HARDWARE PRODUCERS HAVE LOW MARGINAL PRODUCTION COST

- The cost structure for producers of silicon chips is well documented. Chip production is an intensely competitive business with large upfront research and development requirements and low marginal production costs once a chip design is complete. With high fixed costs and low variable operating costs, production volumes are the key to profitability.

- This cost structure has important implications for how manufacturers price their chips. Miners’ capex investment decision tree is based on the expected return on capital as outlined above. We can expect chip vendors to price their chips at a level that will achieve the minimum return profile required by miners to make their investment decision, while also maximizing chip production volumes. As marginal cost on a chip is almost immaterial in relation to the initial research and development expenditure, there is virtually no lower bound to the chip production price.

- During periods adverse to miners, we can expect chip producers to lower the price of chips to almost any level to induce miners to reinvest. Conversely, periods of high demand will see high chip prices.

Parsing the supply and demand dynamics for each input of the Golden Triangle demonstrates that the changes in these variables are largely endogenous and that there is two-way causality between them. The Golden Triangle provides a theoretical framework to understand that various market-driven valves maintain profitability levels at some equilibrium, despite the tremendous volatility in Bitcoin prices.

Implications for Investors

If the Golden Triangle hypothesis holds, it provides a framework to compare miners against one another. Investors should consider the following:

Value operational excellence above all else

Miners are unable to affect price and difficulty levels in a meaningful way. And once chips have been purchased, capital costs are largely sunk. So the main lever mining firms can pull is operational excellence, via efficiencies derived from scale, operational management, and low-cost electricity. Electricity cost is and will remain the most important tool for miners, as its variability is most dramatic.

Survive the winter

As noted, the capital-intensive nature of the business represents a sunk cost and a barrier to exit for many miners. It is possible for the mining industry to move into periods of adverse pricing or extreme difficulty when miners fail to achieve their return-on-capital targets (even if marginal costs are covered). We can expect these miners to exit when their equipment exceeds its useful life. Those exits relieve the pressure on the rest of the industry. In the long term, miners can expect a recovery in their fortunes. But the short-term can be challenging. The implication is that downside-proof business models should be valued over more vulnerable ones. Arrangements such as take-or-pay electricity contracts can be a heavy burden for miners when their marginal cost to produce becomes negative. Resilient business models, such as companies with alternate paths to revenues, should be more highly valued.

Buy the downturn

Mining is capital-intensive, and the ability to procure chips at a competitive price can be the difference between poor and significant returns for investors. In periods of exuberance for cryptocurrency prices, enthusiastic new entrants will give chip producers great bargaining power. Conversely, low interest in the space can be a boon, as it will give buyers purchasing leverage.

The Golden Triangle in Action

Over the last several years, we’ve been able to test the Golden Triangle hypothesis.

As the price of Bitcoin surged (as it did, for example, between the fall of 2020 and the spring of 2021), new miners joined, and difficulty rose to meet the new level of interest.

In these periods of high profitability, chip prices also rose as producers captured their share of excess profits, offsetting the payback period. In periods of low profitability, chip prices fell to compensate for the shift in aggregate demand.

The profitability of the mining market returned to equilibrium over the long term.